A Brief History of TD

The history of the Toronto-Dominion Bank (TD Bank) is a fascinating narrative of growth, resilience, and innovation. Established in 1955 through the merger of the Bank of Toronto and the Dominion Bank, TD Bank has since evolved into one of Canada’s largest and most esteemed financial institutions. Throughout its journey, TD Bank has played a pivotal role in shaping the Canadian banking landscape, pioneering various innovative financial products and services to meet the evolving needs of its customers. With a rich heritage spanning nearly seven decades, TD Bank has continuously adapted to changing economic landscapes and technological advancements, solidifying its position as a trusted financial partner for millions of individuals, businesses, and communities across Canada and beyond. From its humble beginnings to its current status as a global banking leader, the Toronto-Dominion Bank remains committed to its core values of integrity, customer-centricity, and community engagement, driving its ongoing success and prosperity in the ever-changing world of finance.

Who Owns TD Bank?

The Toronto-Dominion Bank, more commonly known as TD Bank, is owned by its shareholders, who own shares in the company. The top 10 shareholders of TD Bank are primarily large institutional investors, including mutual funds, pension funds, and other financial institutions. As of the most recent data available, the top 10 shareholders of TD Bank are as follows:

1. The Vanguard Group, Inc.

2. Royal Bank of Canada

3. BlackRock, Inc.

4. Canada Pension Plan Investment Board

5. Fidelity Investments

6. TD Asset Management Inc.

7. Bank of Montreal

8. CIBC Asset Management Inc.

9. RBC Global Asset Management Inc.

10. National Bank of Canada

These shareholders collectively hold a significant portion of TD Bank’s outstanding shares, and therefore have a significant ownership interest in the company.

TD Mission Statement

The Toronto-Dominion Bank’s mission statement is centered around providing exceptional and personalized customer experiences while also delivering innovative financial solutions to help clients achieve their financial goals. The bank is committed to being a trusted and responsible financial institution that contributes to the well-being and prosperity of the communities it serves. TD Bank’s mission is also focused on fostering a diverse and inclusive workplace that values and respects individuals and supports their professional growth and development.

How Does TD Make Money?

The Toronto-Dominion Bank, commonly known as TD Bank, employs a business model that generates revenue primarily from its financial services. The bank makes money through a variety of sources, including interest and fees from lending activities such as mortgages, loans, and credit cards. TD Bank also earns income from its investing and asset management services, as well as from transaction fees and service charges. Additionally, the bank gains revenue from its insurance and wealth management products. Overall, TD Bank’s diversified revenue streams contribute to its overall financial strength and stability.

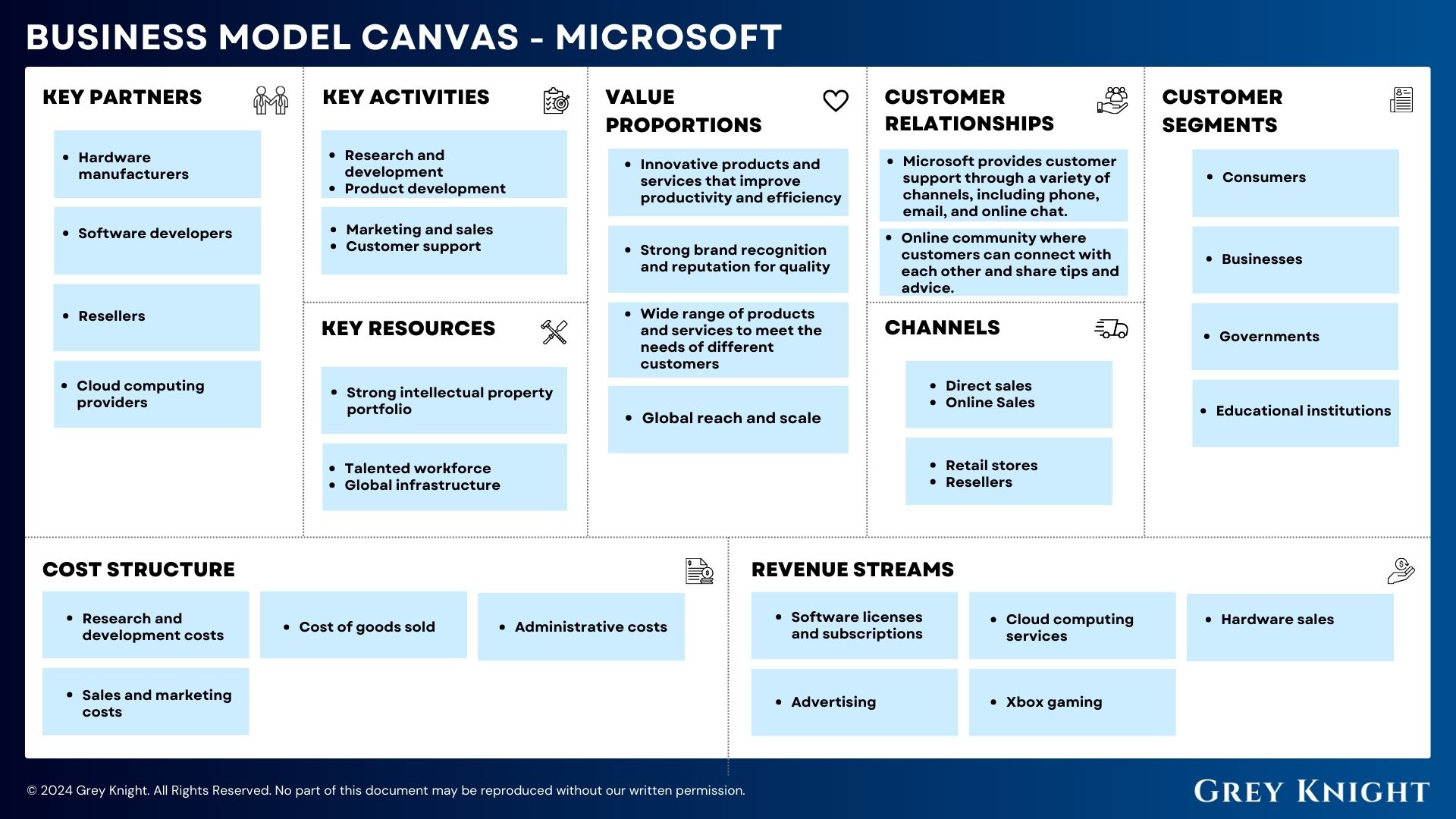

TD Business Model Canvas

The Business Model Canvas is a strategic management tool that allows businesses to describe, design, challenge, invent, and pivot their business model. It provides a visual representation of how a company creates, delivers, and captures value. This tool is essential for understanding your business model and identifying any weaknesses or areas of improvement.

1. Customer Segments:

– Retail Banking Customers: Individuals who use TD Bank’s various financial services such as checking and savings accounts, credit cards, loans, and mortgages.

– Small Business Customers: Businesses including small to medium-sized enterprises (SMEs) that require banking services and financial solutions.

– Corporate and Institutional Clients: Larger corporations, government agencies, and institutional investors that need commercial banking and capital markets expertise.

2. Value Propositions:

– Convenient Banking: Easy access to banking services through online and mobile platforms, as well as a network of branches and ATMs.

– Financial Solutions: Offering a wide range of financial products and services tailored to meet the needs of individual and business clients.

– Trust and Security: Providing a secure and trusted banking experience for customers, ensuring the safety and privacy of their financial information.

3. Channels:

– Branches: Physical locations where customers can access banking services, consult with financial advisors, and conduct transactions.

– Online and Mobile Banking: Digital platforms that allow customers to manage their accounts, pay bills, transfer funds, and apply for new products and services.

– Call Centers: Customer service representatives available to assist clients with inquiries, account management, and issue resolution.

4. Customer Relationships:

– Personalized Service: Engaging with customers to understand their financial goals and needs, and providing personalized recommendations and solutions.

– Customer Support: Offering ongoing support and assistance to address any concerns or issues, and to maintain a positive relationship with customers.

– Loyalty Programs: Rewarding customers for their continued patronage through loyalty programs, perks, and exclusive offers.

5. Revenue Streams:

– Interest Income: Generating revenue from interest earned on loans, mortgages, and other interest-bearing assets.

– Service Fees: Charging fees for various banking services such as account maintenance, overdrafts, wire transfers, and foreign currency transactions.

– Investment and Advisory Fees: Earning fees from providing investment management and financial advisory services to clients.

6. Key Resources:

– Financial Capital: Access to capital to fund lending activities, provide liquidity, and maintain regulatory capital requirements.

– Technology: Utilizing advanced banking technology and digital infrastructure to deliver efficient and innovative banking solutions.

– Skilled Workforce: Employing a skilled and knowledgeable workforce to provide high-quality customer service, financial advice, and risk management.

7. Key Activities:

– Lending and Credit Services: Providing loans, mortgages, credit lines, and other credit products to individual and business clients.

– Risk Management: Assessing and managing various types of financial risks including credit risk, market risk, and operational risk.

– Regulatory Compliance: Ensuring compliance with industry regulations, banking laws, and government mandates.

8. Key Partners:

– Regulatory Authorities: Collaborating with regulatory bodies to comply with financial regulations, laws, and industry standards.

– Technology Providers: Partnering with technology companies to leverage cutting-edge banking technologies, software, and digital solutions.

– Marketing and Advertising Agencies: Engaging with marketing and advertising partners to promote TD Bank’s brand, products, and services.

9. Cost Structure:

– Personnel Expenses: Costs associated with employee salaries, benefits, training, and development.

– Technology and Infrastructure: Investments in technology, digital infrastructure, and IT systems to support banking operations and customer experience.

– Compliance and Legal: Expenses related to regulatory compliance, legal counsel, and risk management activities.

The Toronto-Dominion Bank, commonly known as TD Bank, faces tough competition in the financial industry. Its top competitors include the Bank of Montreal, Royal Bank of Canada, Scotiabank, CIBC, and HSBC Bank Canada. These competitors offer similar banking and financial services, and are also major players in the Canadian and international financial markets. TD Bank must continuously innovate and provide exceptional customer service to stay ahead of these capable rivals.

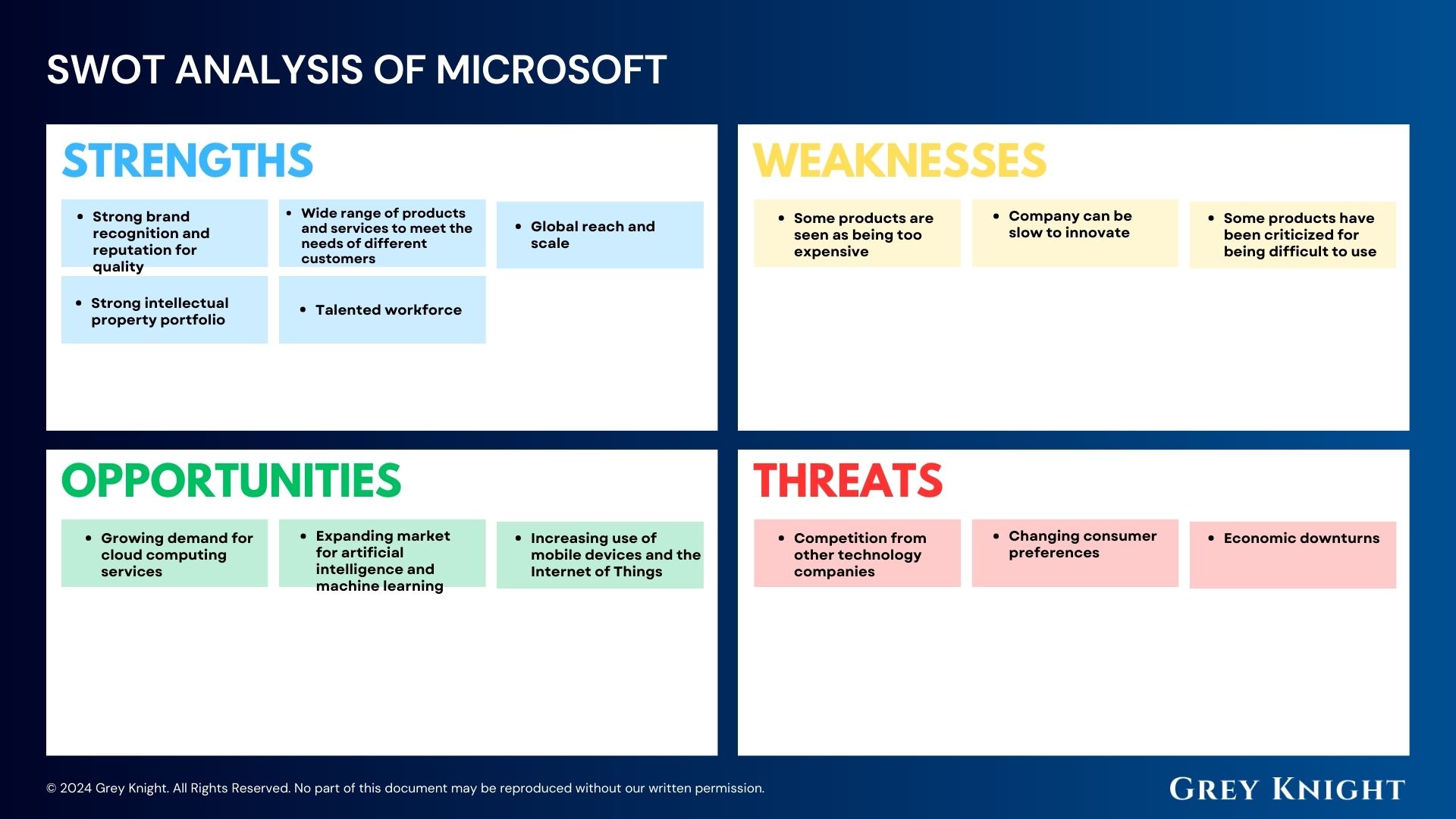

TD SWOT Analysis

Strengths:

1. Strong brand recognition and reputation in the banking industry

2. Diversified business operations in both retail and commercial banking

3. Large customer base and widespread presence in Canada and the U.S.

4. Robust digital banking platform and technology integration

5. Strong financial performance and stability

Weaknesses:

1. Vulnerability to economic downturns and interest rate fluctuations

2. Limited presence in international markets compared to some competitors

3. High reliance on mortgage and consumer lending

Opportunities:

1. Expansion into emerging markets and untapped demographic segments

2. Adoption of advanced technologies to enhance customer experience

3. Potential for acquisitions and mergers to further strengthen market share

Threats:

1. Intense competition from other financial institutions and non-traditional players

2. Regulatory changes and compliance requirements

3. Economic instability and geopolitical events

4. Increasing cybersecurity threats and data breaches.

Concluding Analysis

In conclusion, The Toronto-Dominion Bank has successfully implemented a strong and diverse business model that has enabled it to navigate through economic uncertainties and adapt to changing industry trends. As an analyst, I am optimistic about the future of the bank. With its robust digital strategy, continued focus on innovation, and commitment to customer-centric solutions, I believe The Toronto-Dominion Bank is well-positioned to capitalize on emerging opportunities and maintain its position as a leader in the financial services industry. I have confidence in the bank’s ability to drive sustainable growth and deliver value to its stakeholders in the years ahead.

Additional Resources

To keep learning and advancing your career, we highly recommend these additional resources:

Business Model Canvas of The Top 1,000 Largest Companies by Market Cap in 2024

A List of 1000 Venture Capital Firms & Investors with LinkedIn Profiles

Peter Thiel and the 16 Unicorns: The Legacy of Thiel Fellowship