A Brief History of Visa

Visa was founded in 1958 as BankAmericard, the first successful credit card program in the United States. It was created by Bank of America as a way to provide its customers with a convenient method of payment. In 1976, BankAmericard officially became Visa, and the company began to expand internationally.

Visa went public in 2008, becoming a publicly traded company on the New York Stock Exchange. Over the years, Visa has grown to become one of the largest and most recognizable payment technology companies in the world, with a global network that processes billions of transactions every year.

Today, Visa continues to innovate and develop new technologies to make payments faster, more secure, and more convenient for consumers and businesses worldwide. The company has expanded its services to include digital payments, mobile payments, and other cutting-edge payment solutions, solidifying its position as a leader in the financial technology industry.

Who Owns Visa?

Visa is a publicly traded company, which means that it is owned by its shareholders. The largest shareholders of Visa are institutional investors, such as mutual funds and pension funds, as well as individual investors who own shares of the company. As of the latest available data, the top 10 shareholders of Visa are:

1. The Vanguard Group

2. BlackRock

3. State Street Corporation

4. Fidelity Management & Research Company

5. Wellington Management Company, LLP

6. T. Rowe Price Associates

7. Capital Group Companies

8. The California Public Employees’ Retirement System

9. Northern Trust Corporation

10. Massachusetts Financial Services Company

These institutional investors and investment management firms hold significant stakes in Visa and play a key role in the company’s ownership and direction.

Visa Mission Statement

Visa’s mission statement is to connect the world through innovative payment solutions that enable individuals, businesses, and economies to thrive. They are committed to providing secure, reliable, and convenient ways for people to make transactions, from everyday purchases to large-scale investments. Their goal is to continuously improve and expand their services to meet the evolving needs of global commerce and empower financial inclusion for all.

How Visa Makes Money?

Visa operates as a payments technology company that facilitates electronic funds transfers across the globe. The company’s primary revenue streams come from transaction fees charged to merchants and financial institutions for the use of its payment network. Visa also generates revenue from data processing fees, international transaction fees, and other service fees. Additionally, the company earns income from interest on its account balances and investments, as well as from various other services such as consulting, risk management, and fraud detection. Overall, Visa’s business model is centered around providing secure and efficient payment solutions while monetizing its network through a variety of transaction and service fees.’s Business Model Canvas

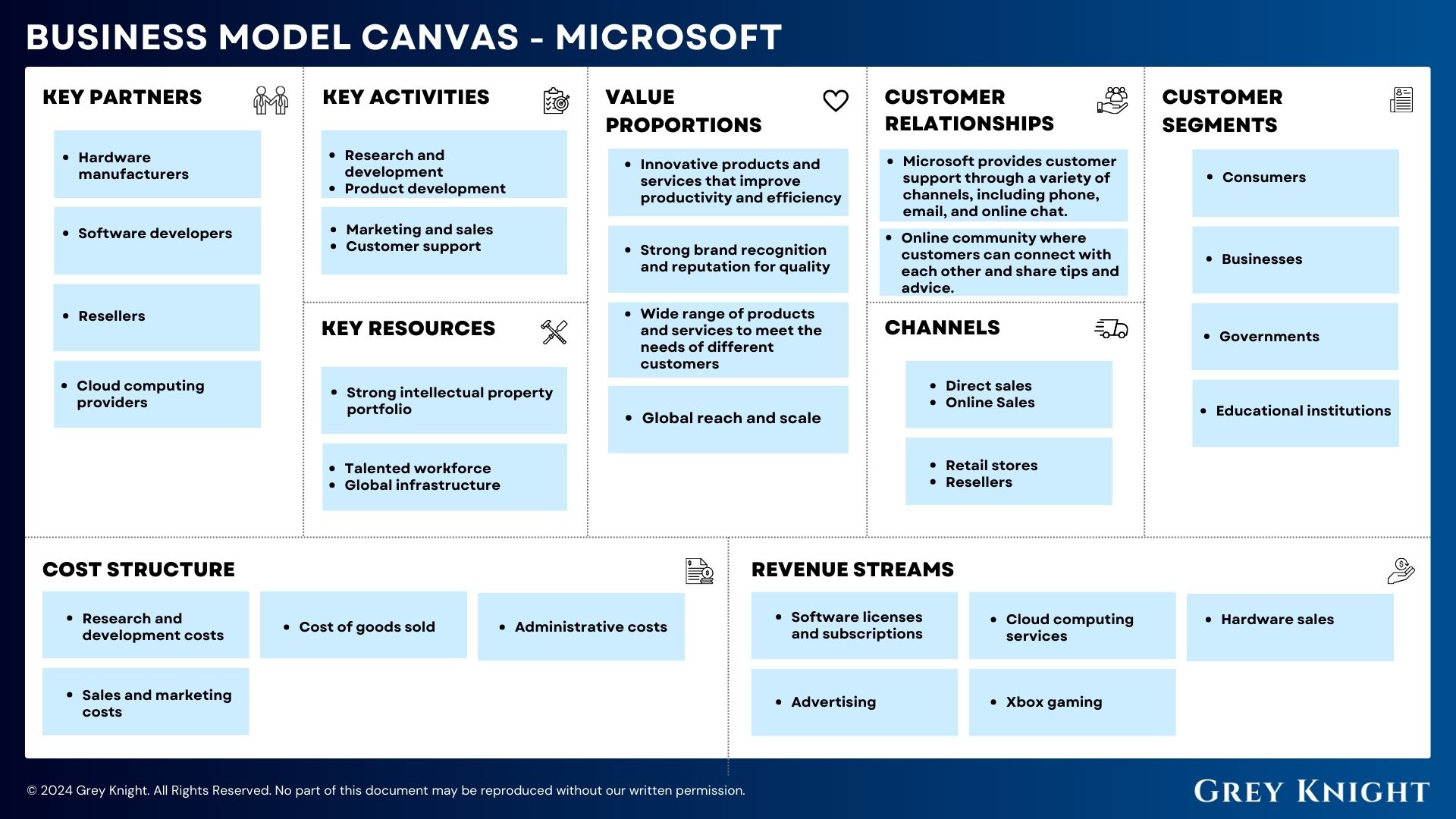

Visa’s Business Model Canvas

The business model canvas is a strategic management tool that provides a visual overview of an organization’s key components and how they interact with each other. It consists of nine building blocks that include customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure. This framework gives businesses a clearer understanding of their operations and helps to identify areas for improvement and innovation. In this section, we will provide a detailed Business Model Canvas for Visa.

Customer Segments:

1. Financial institutions

2. Merchants

3. Governments

4. Cardholders

5. Businesses

Value Propositions:

1. Secure and reliable payment system

2. Global Acceptance

3. Fraud protection

4. Innovative technology solutions

5. Assistance with regulatory compliance

Channels:

1. Financial institutions

2. Online and mobile platforms

3. Sales and marketing teams

4. Strategic partnerships

5. Retail locations

Customer Relationships:

1. Customer support services

2. Education and training programs

3. Account management

4. Loyalty programs

5. Community engagement initiatives

Revenue Streams:

1. Transaction fees

2. Licensing and service fees

3. Interest income

4. Cross-border transaction fees

5. Data analytics and insights

Key Resources:

1. Global network infrastructure

2. Data centers and security systems

3. Brand Reputation

4. Technology and innovation

5. Regulatory and compliance expertise

Key Activities:

1. Payment processing

2. Research and development

3. Risk management

4. Regulatory compliance

5. Marketing and sales

Key Partners:

1. Financial institutions

2. Merchants and businesses

3. Technology companies

4. Government agencies

5. Industry associations

Cost Structure:

1. Technology and infrastructure

2. Compliance and regulatory costs

3. Marketing and sales expenses

4. Employee salaries and benefits

5. Research and development investment

Visa’s Competitors

Visa operates in a competitive market with several key players vying for market share in the global payments industry. Its top competitors include Mastercard, American Express, PayPal, UnionPay, and Discover Financial Services. Each of these companies offers a range of payment solutions and services and competes with Visa in various regions and sectors of the market. The ongoing battle for dominance in the payments industry ensures that Visa must continue to innovate and provide top-notch products and services to maintain its position as a leading player in the industry.

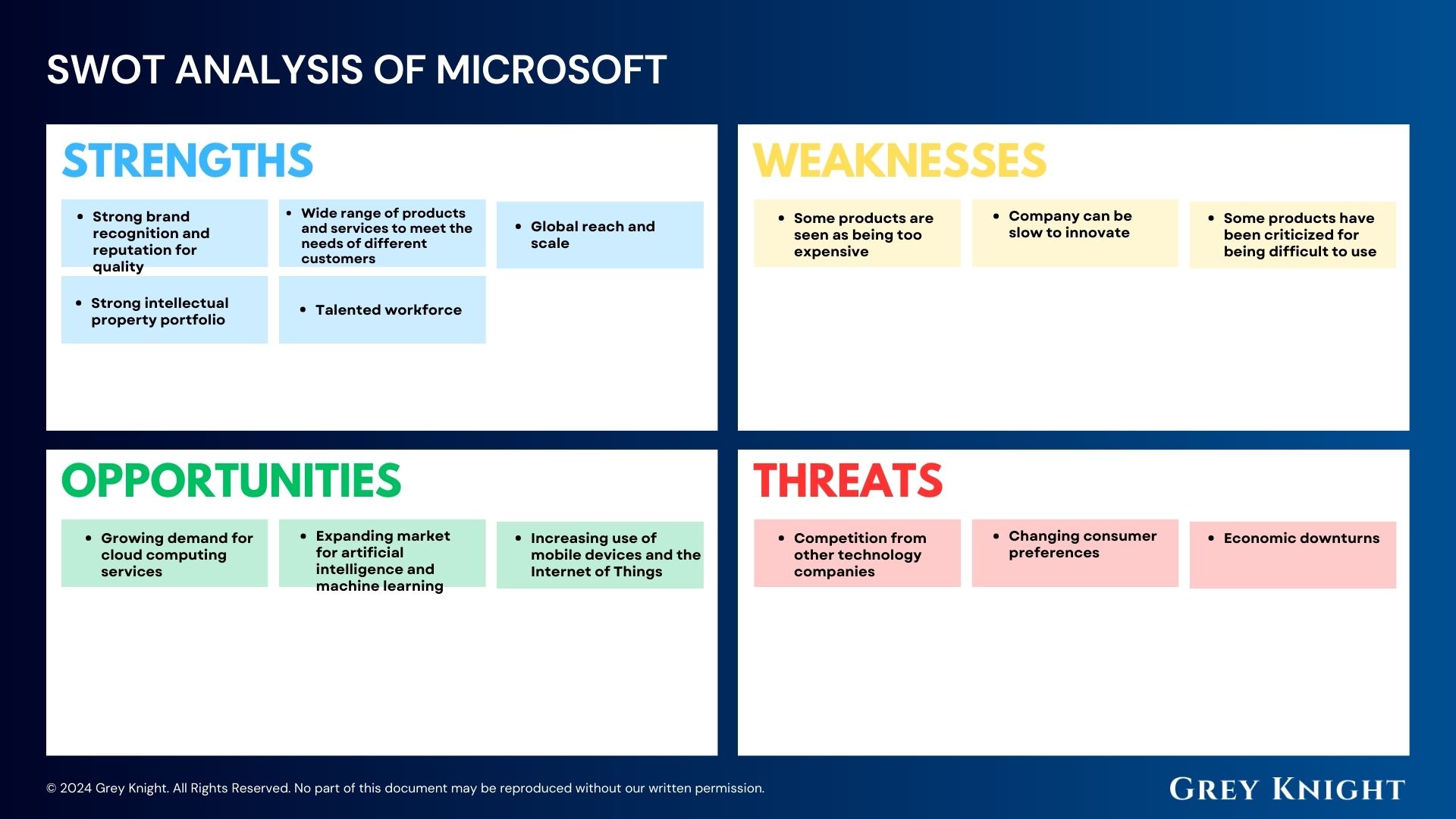

Visa’s SWOT Analysis

Strengths:

1. Global brand recognition and presence

2. Strong and secure payment processing technology

3. Diversified product offerings in credit, debit, and prepaid cards

4. Extensive network of partners and clients

Weaknesses:

1. Dependency on external financial market conditions

2. Reliance on government regulations for operation

3. Vulnerability to technological disruptions and cybersecurity threats

Opportunities:

1. Growth potential in emerging markets

2. Expansion of digital payment solutions

3. Increase in contactless and mobile payment adoption

Threats:

1. Intense competition from other payment processing companies

2. Regulatory changes impacting fees and interchange rates

3. Economic downturns affecting consumer spending habits

Concluding Analysis

In wrapping up my analysis of Visa’s business model, it’s clear that the company’s focus on technological innovation and adaptability has positioned it as a leader in the digital payments space. With the global shift towards cashless transactions and the increasing reliance on e-commerce, Visa’s strong financial performance and strategic partnerships indicate a promising future. As an analyst, I believe that Visa’s continued investments in digital infrastructure and its commitment to providing secure, convenient payment solutions will drive its long-term success. The company’s ability to navigate evolving consumer preferences and regulatory landscapes will be key in sustaining its competitive edge. Overall, I am optimistic about Visa’s potential for continued growth and industry leadership.

Additional Resources

To keep learning and advancing your career, we highly recommend these additional resources:

Business Model Canvas of The Top 1,000 Largest Companies by Market Cap in 2024

A List of 1000 Venture Capital Firms & Investors with LinkedIn Profiles

Peter Thiel and the 16 Unicorns: The Legacy of Thiel Fellowship